Starting a trucking business is an exciting venture that offers independence and the potential for significant income. However, when you start a trucking business, managing taxes and compliance is just as critical as maintaining your equipment and securing profitable freight. Many new owner-operators focus heavily on the operational side, buying a truck, getting insurance, and finding loads, but overlook the complex web of federal and state tax obligations. Missing a tax filing or failing to maintain proper records can quickly sideline your registration, trigger audits, or drain your cash flow.

This comprehensive guide is designed specifically for new owner-operators and small fleet startups. We will focus on the essential tax obligations you will face in your first year, including the Heavy Vehicle Use Tax, the International Fuel Tax Agreement, federal income tax, and quarterly estimated payments. By establishing a solid foundation before you haul your first load, you can protect your margins and build a sustainable business. We have also included a practical compliance checklist to serve as your companion resource throughout the year.

What Are the Essential Business and Tax Setup Steps in the First 30 to 60 Days?

Before you hit the road, you must establish the legal and financial framework of your new trucking company. These initial decisions will dictate how your profits are taxed and how much administrative work you will need to handle.

Choose a Legal and Tax Structure

One of the first decisions you must make is choosing a business structure. The most common options for owner-operators are Sole Proprietorship, Limited Liability Company, S Corporation, and C Corporation.

- Sole Proprietorship: This is the simplest structure, but it offers no personal liability protection. Your business profits are reported on your personal tax return and are fully subject to self-employment tax.

- LLC: An LLC provides personal liability protection, separating your personal assets from your business liabilities. By default, a single-member LLC is taxed like a sole proprietorship, but it offers flexibility in how you choose to be taxed later.

- S Corp: An LLC can elect to be taxed as an S Corp. This structure can provide significant tax savings for profitable trucking businesses because it allows you to split your income into a reasonable salary (subject to payroll taxes) and distributions (not subject to self-employment tax). However, it requires more complex payroll administration.

- C Corp: A C Corp is a separate taxable entity. It pays corporate income tax, and owners are taxed again on dividends (double taxation). This is generally less common for single owner-operators.

When choosing a structure, consider your liability risks, the complexity of payroll administration, and your long-term growth plans.

Get Your EIN and Open Business Accounts

Once your entity is formed, obtain an Employer Identification Number from the IRS. This is essentially a social security number for your business and is required for opening bank accounts and filing certain taxes.

It is absolutely crucial to open separate business checking and savings accounts. Commingling personal and business funds is a fast track to an audit and can pierce the corporate veil of your LLC. Additionally, establish a dedicated tax reserve account. Every time you receive a settlement, transfer a percentage (e.g., 20-25%) into this account to cover your quarterly estimated taxes, HVUT, and other liabilities.

Register for IFTA and IRP if Operating Interstate

If you plan to operate across state lines with a vehicle weighing over 26,000 pounds or having three or more axles, you must register for the International Fuel Tax Agreement and the International Registration Plan.

- IFTA: Simplifies the reporting of fuel use taxes by allowing you to report to your base jurisdiction, which then distributes the taxes to the states where you traveled.

- IRP: Allows you to pay apportioned registration fees based on the miles driven in each jurisdiction.

You will register for both through your base jurisdiction (usually your home state).

Set Up Your Accounting Framework

A solid accounting system is your best defense against tax season stress. Create a Chart of Accounts tailored specifically to trucking. Key categories should include:

- Fuel

- Repairs and Maintenance

- Permits and Licenses

- Tolls

- Insurance

- Depreciation

- Driver Pay (if applicable)

Decide whether you will use cash or accrual accounting (most owner-operators use cash basis) and establish a strict monthly close routine to reconcile your accounts.

| Accounting Method | Description | Best For |

|---|---|---|

| Cash Basis | Records income when received and expenses when paid. | Most single owner-operators; simpler tracking. |

| Accrual Basis | Records income when earned and expenses when incurred, regardless of cash flow. | Growing fleets; provides a better picture of long-term profitability. |

How Are Federal Income and Self-Employment Taxes Handled for Owner-Operators?

Transitioning from a company driver (receiving a W-2) to an owner-operator means taking full responsibility for your income and self-employment taxes. Understanding how these taxes work is critical to staying current in your first year.

How Profits Are Taxed by Entity Type

If you operate as a Sole Proprietor or a single-member LLC, your trucking business profits are reported on Schedule C of your personal Form 1040. The net profit is subject to ordinary income tax. If you operate as a partnership or an S Corp, the business itself does not pay federal income tax. Instead, the profits “pass-through” to the owners’ personal tax returns. A C Corp files its own corporate tax return and pays taxes at the corporate rate.

Self-Employment Tax and Payroll Interactions

As an independent contractor, you are responsible for both the employer and employee portions of Social Security and Medicare taxes, collectively known as the self-employment tax (currently 15.3%). If you operate as a Sole Proprietor or a standard LLC, this tax applies to your entire net profit.

If you elect S Corp taxation, the rules change. You must pay yourself a “reasonable salary” through a formal payroll system. This salary is subject to standard payroll taxes. The remaining profit can be taken as an owner’s draw or distribution, which is not subject to self-employment tax. This strategy can save thousands of dollars annually, but it requires strict compliance with payroll reporting.

Quarterly Estimated Taxes

Because no one is withholding taxes from your settlements, the IRS requires you to make quarterly estimated tax payments if you expect to owe $1,000 or more when your return is filed.

The due dates for these payments are typically:

- April 15

- June 15

- September 15

- January 15 (of the following year)

To avoid underpayment penalties, you can use the “safe harbor” rule: pay 100% of the tax shown on your previous year’s return (or 110% if your adjusted gross income was over $150,000). Alternatively, you can use a simple projection method by analyzing your year-to-date net profit and estimating your annualized income.

State Income and Franchise Taxes

Do not forget about state taxes. Depending on where your business is registered and where you operate, you may owe state income taxes or franchise taxes. Even if you incorporate in a tax-friendly state like Nevada or Wyoming, you generally still have to pay taxes in the state where you actually live and conduct business.

What Is the Heavy Vehicle Use Tax and How Do I File Form 2290?

The Heavy Vehicle Use Tax is an annual federal tax assessed on heavy vehicles operating on public highways. Failing to file and pay this tax will prevent you from renewing your vehicle registration or IRP plates.

Who Owes HVUT and When Is It Due?

You owe HVUT if you operate a highway motor vehicle with a taxable gross weight of 55,000 pounds or more. The tax year runs from July 1 to June 30. The annual filing deadline is August 31 for vehicles in use during July.

If you purchase a new or used truck later in the year, the tax is prorated based on the month of first use. The deadline is the last day of the month following the month of first use. For example, if you buy a truck and put it on the road in October, your Form 2290 is due by November 30.

Suspended Vehicles and Special Cases

If you expect to drive your vehicle fewer than 5,000 miles (or 7,500 miles for agricultural vehicles) during the tax year, you can claim a suspension of the tax. You still must file Form 2290, but you will not owe a payment. If you later exceed the mileage limit, the tax becomes due. Special rules also apply if the taxable weight of your vehicle changes, or if the vehicle is sold or destroyed during the year.

What You Need to File Form 2290

To file your Form 2290, you will need:

- Your Employer Identification Number

- The Vehicle Identification Number of each truck

- The taxable gross weight of each vehicle

- The month of first use

- A payment method

Penalties and Common Mistakes

Late filing of Form 2290 incurs a penalty of 4.5% of the total tax due, assessed monthly for up to five months, plus a late payment penalty of 0.5% per month and interest charges.

Common mistakes include:

- Entering an incorrect VIN (which will cause your registration renewal to be rejected).

- Using a Social Security Number instead of an EIN.

- Failing to retain the stamped Schedule 1, which serves as your official proof of payment for the DMV.

How Do Fuel and Distance Taxes Like IFTA and IRP Work?

Ongoing fuel and distance reporting can be a significant administrative burden for new carriers. Understanding these requirements is essential to avoid costly audits and penalties.

IFTA Basics

The International Fuel Tax Agreement simplifies fuel tax reporting for interstate carriers. Instead of obtaining fuel permits for every state you enter, you file one quarterly return with your base jurisdiction.

You must report the total miles driven and the total gallons of fuel purchased in each participating jurisdiction. The IFTA system calculates whether you owe additional tax (if you drove extensively in a high-tax state but bought fuel in a low-tax state) or if you are owed a credit.

IFTA Deadlines:

- Q1 (Jan-Mar): April 30

- Q2 (Apr-Jun): July 31

- Q3 (Jul-Sep): October 31

- Q4 (Oct-Dec): January 31

IRP Apportionment

The International Registration Plan is an agreement that allows you to pay apportioned registration fees based on the percentage of miles you drive in each jurisdiction. When you first register, you will estimate your mileage. In subsequent years, your renewal fees will be based on your actual reported mileage from the previous reporting period. This requires meticulous mileage tracking to ensure you are not overpaying.

Weight-Distance Taxes in Certain States

In addition to IFTA, a few states impose separate weight-distance or highway use taxes. These taxes are typically based on the vehicle’s weight and the miles driven within that specific state. States with notable weight-distance taxes include:

- New York (HUT)

- Kentucky (KYU)

- New Mexico (WDT)

- Oregon (WMT)

If you operate in these states, you must obtain the necessary permits and file separate periodic returns.

Record Requirements and Audits

IFTA and IRP audits are common and rigorous. You must maintain detailed records to support your returns. This includes:

- Individual vehicle mileage records (trip sheets or ELD exports) showing routes, state lines crossed, and odometer readings.

- Original fuel receipts showing the date, location, gallons purchased, fuel type, and vehicle unit number.

Ensure your ELD mileage reconciles perfectly with your fuel receipts and your quarterly filings.

What Are the Tax Implications of Paying Drivers or Hiring Help?

If your business grows and you decide to add drivers or hire administrative help, you must navigate complex worker classification and payroll tax rules.

Worker Classification: Employees vs. 1099 Contractors

Misclassifying workers is one of the most significant risks in the trucking industry. The IRS and Department of Labor strictly scrutinize whether a driver is a W-2 employee or a 1099 independent contractor.

- Employee (W-2): You control how, when, and where the work is done. You provide the equipment (the truck) and cover the operating expenses.

- Independent Contractor (1099): The worker controls their schedule, uses their own equipment (or leases it under a true lease), and bears the risk of profit or loss.

If you own the truck and dictate the driver’s schedule, they are almost certainly an employee.

Payroll Taxes and Filings for Employees

If you hire W-2 employees, you must withhold federal and state income taxes, as well as the employee’s share of FICA (Social Security and Medicare). You are also responsible for paying the employer’s share of FICA, federal unemployment tax, and state unemployment insurance. You must issue W-2 forms to your employees by January 31 of the following year.

Reporting for Contractors

If you legitimately hire independent contractors (e.g., owner-operators leased to your authority), you must collect a Form W-9 from them before they start work. If you pay them $600 or more during the year, you must issue them a Form 1099-NEC by January 31. Failure to collect a W-9 may require you to perform backup withholding on their payments.

Per Diem for Drivers

Per diem is a tax deduction for meals and incidental expenses incurred while traveling away from home overnight for business. The transportation industry has special, higher per diem rates. Currently, you can deduct 80% of the standard per diem rate for days spent over the road. To claim this deduction, you must keep contemporaneous logs showing the dates, locations, and business purpose of the travel.

How Can I Maximize Deductions, Depreciation, and Understand My Cost Per Mile?

To run a profitable trucking business, you must aggressively track every legitimate business expense and understand how those expenses impact your cost per mile.

Everyday Operating Deductions

As an owner-operator, almost everything related to operating your truck is deductible. Key deductions include:

- Fuel and DEF

- Repairs, maintenance, and parts

- Insurance premiums

- Tolls, scales, and parking fees

- Permits and licenses

- Factoring fees and bank charges

- Communications

- Interest on your truck loan

Depreciation of Tractors and Trailers

Depreciation allows you to recover the cost of large assets, like your truck and trailer, over time. Tractors are typically depreciated over 3 years, and trailers over 5 years, using the MACRS (Modified Accelerated Cost Recovery System) schedule.

Alternatively, you may be eligible to use Section 179 expensing or Bonus Depreciation to deduct a large portion (or all) of the purchase price in the first year. Note that Bonus Depreciation rules are currently phasing down, so consult with a tax professional to determine the most advantageous strategy for your specific tax situation.

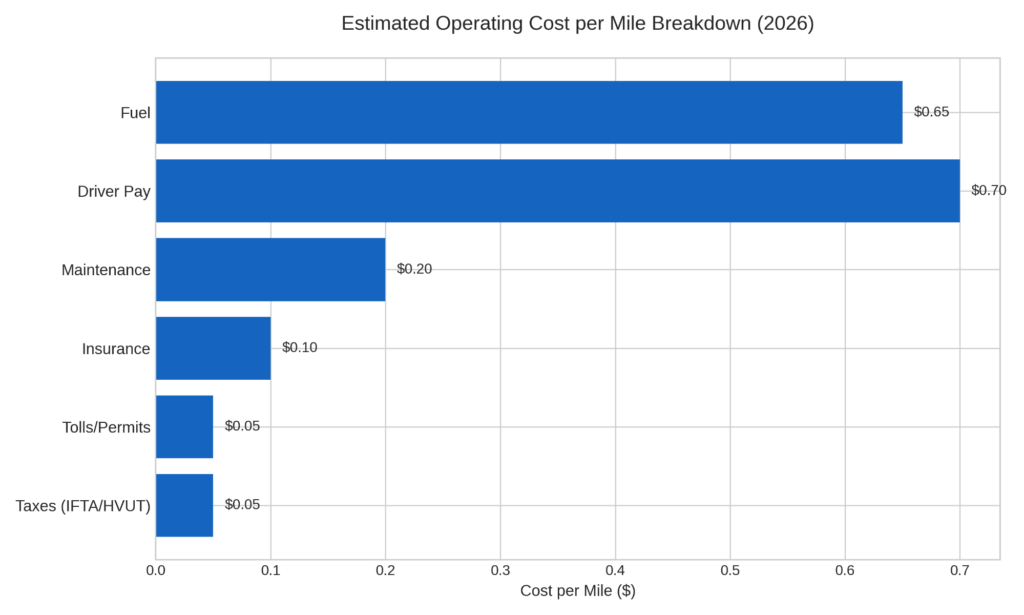

Tracking Cost Per Mile

Understanding your cost per mile is the foundation of profitable freight pricing. To calculate it, divide your total expenses (fixed + variable) by the total miles driven.

By tying your expenses and tax savings to your pricing decisions, you can ensure that every load you haul contributes to your bottom line and covers your tax liabilities.

How Do I Build a Recordkeeping System That Survives an Audit?

Good recordkeeping is not just about tax preparation; it is about protecting your business in the event of an audit. Translating complex rules into a daily and monthly routine is essential.

What to Keep and for How Long

Different agencies have different retention requirements:

- IRS Income Tax Records: Generally, keep returns and supporting documents for at least 3 years (or up to 7 years in certain circumstances).

- IFTA and IRP Records: Keep mileage logs, trip sheets, and fuel receipts for at least 4 years.

- HVUT Records: Retain your stamped Schedule 1 and proof of payment for at least 3 years.

Linking ELD, Fuel, and Maintenance Data

Your records must tell a consistent story. An auditor will look to see if your ELD mileage matches the miles reported on your IFTA returns. They will check if the fuel gallons claimed on IFTA match your actual fuel receipts. Ensure that Bills of Lading, trip sheets, and maintenance records all align with the dates and locations of your reported travel.

A Monthly Close Checklist

Implement a strict monthly routine to keep your books clean:

- Reconcile your bank and credit card statements.

- Reconcile your fuel card statements and verify all receipts are saved.

- Review Accounts Payable (bills to pay) and Accounts Receivable (unpaid invoices).

- Record any depreciation or adjusting entries.

- Transfer the calculated percentage of income to your tax reserve account.

- Identify and track down any missing receipts or BOLs.

We highly recommend using a digital storage system with consistent file naming conventions (e.g., 2026_04_Fuel_Receipts.pdf).

What Does an Annual and Quarterly Compliance Calendar Look Like?

To prevent missed deadlines and late fees, you need a consolidated timeline of your obligations.

Quarterly Cadence

- Estimated Income Tax: Due April 15, June 15, September 15, and January 15.

- IFTA Returns: Due the last day of the month following the end of the quarter (April 30, July 31, October 31, January 31).

- State Filings: Check your state for specific quarterly weight-distance or sales tax deadlines.

Annual Cycle

- January: Issue W-2s and 1099s by January 31. Q4 IFTA and Q4 Estimated Taxes due.

- March/April: Business and personal income tax returns due (dates vary by entity type).

- July/August: New HVUT tax year begins July 1. Form 2290 due August 31.

- Varies: IRP renewal (deadlines vary by state and registration date).

Practical Workflow

Create a 12-month calendar and set digital reminders 30 days before every major due date. Assign specific tasks to yourself, your spouse, or your back-office provider, and review the calendar at the start of every month.

Frequently Asked Questions (FAQ): How Do I Start a Trucking Business

What taxes do I pay when starting a trucking business?

When starting a trucking business, you are responsible for federal and state income taxes, self-employment taxes (Social Security and Medicare), the Heavy Vehicle Use Tax, IFTA fuel taxes, and potentially state-specific weight-distance taxes. If you hire employees, you will also owe payroll taxes.

Do I need IFTA if I only run in one state?

No, if you operate exclusively within the borders of a single state (intrastate commerce), you do not need to register for IFTA. You simply pay the fuel tax at the pump in your home state.

When is HVUT due for a newly purchased truck?

For a newly purchased truck, the HVUT Form 2290 is due by the last day of the month following the month you first use the vehicle on public highways. For example, if you start driving the truck in October, the tax is due November 30.

How are owner-operators taxed compared with S corps?

A standard owner-operator (Sole Proprietor or LLC) pays self-employment tax on their entire net business profit. An owner-operator who elects S Corp status pays themselves a reasonable salary (subject to payroll taxes) and takes the remaining profit as a distribution, which is not subject to self-employment tax, potentially saving money.

What records are required for an IFTA audit?

For an IFTA audit, you must provide individual vehicle mileage records (like ELD exports or detailed trip sheets) showing routes and state lines crossed, along with original fuel receipts showing the date, location, gallons, fuel type, and truck unit number.

Can I claim per diem and actual meal receipts at the same time?

No, you must choose one method for the entire tax year. You can either claim the standard transportation industry per diem rate for days away from home overnight, or you can deduct your actual, receipted meal expenses. Most drivers find the per diem method simpler and more beneficial.