Owning a truck can raise your earning ceiling, but it also moves you from being only a driver to being a business operator. The truck you buy affects the lanes you can serve, the freight you can accept, the financing you can qualify for, and the amount of downtime you can absorb. That is why the smartest buyers do not begin with inventory listings. They begin with a plan.

If you are trying to understand how to purchase a semi truck, this article walks through the full decision path from business model to compliance. You will see how to compare lease-on and own-authority models, estimate total cost of ownership, review financing and down-payment expectations, inspect used equipment, and finish registration and insurance without missing the steps that often delay first-time buyers.

A Truck Buyer’s Guide

A truck buyers guide is a practical framework that helps you make a truck purchase in the right order instead of making an emotional decision from a listing photo. For a first-time owner-operator, that structure matters because the truck has to fit your freight, budget, and compliance plan at the same time. FMCSA makes clear that business type, safety registration, and operating authority obligations are tied to how you plan to operate, not just to the truck you buy [1] [2].

The simplest way to shorten the learning curve is to treat the purchase as seven phases: plan, qualify, search, inspect, insure, register, and operate. In the planning phase, you define whether you will lease on to a carrier or run under your own authority. In the qualification phase, you organize your business documents, credit profile, and down payment. Only then should you shop and inspect trucks.

Your operating model should drive the entire purchase. If you lease on to an established carrier, you may gain easier access to freight, fuel programs, and compliance support, but you may also give up some revenue upside and dispatch freedom. If you operate under your own authority, you gain more control over lanes, customer relationships, and rate-setting, but you also take on more responsibility for insurance, filings, safety systems, and cash reserves. FMCSA notes that interstate for-hire carriers transporting federally regulated commodities generally need both a USDOT number and operating authority, while the type of authority requested affects insurance and financial responsibility requirements [2].

Freight type matters just as much as business structure. Long-haul dry van work, regional refrigerated lanes, flatbed freight, and heavy haul all place different demands on engine torque, wheelbase, axle ratio, fuel capacity, and driver comfort. If you plan to run mostly regional freight with frequent stops, the truck that makes sense may not be the same truck that works for coast-to-coast sleeper operations. Before you set a budget, write down your target freight, your usual gross weight, the regions you plan to cover, and whether shippers or carriers in your network prefer certain specifications.

You should also treat business setup as part of the buying decision. SBA guidance for business planning and financing emphasizes that equipment purchases are easier to support when you can explain your operating model, revenue path, and repayment capacity [3]. That means forming the right business entity, getting an EIN, setting up bookkeeping, and deciding how you will track maintenance, fuel, settlements, taxes, and quarterly estimates before the truck ever hits the road.

What should your budget and total cost of ownership look like?

The truck price is only the first number. The smarter number is your total cost of ownership, or TCO, because it combines acquisition cost with the recurring expenses that decide whether your truck will be profitable. Buyers who focus only on the monthly payment often end up underestimating the real cash they need to survive the first six months.

Start with acquisition costs. Those usually include the down payment, sales tax where applicable, title fees, registration fees, dealer documentation charges, and any immediate repairs or preventive maintenance you want completed before the first load. A used truck that looks cheaper on paper can become more expensive in week one if it needs tires, batteries, brakes, or aftertreatment work immediately after purchase.

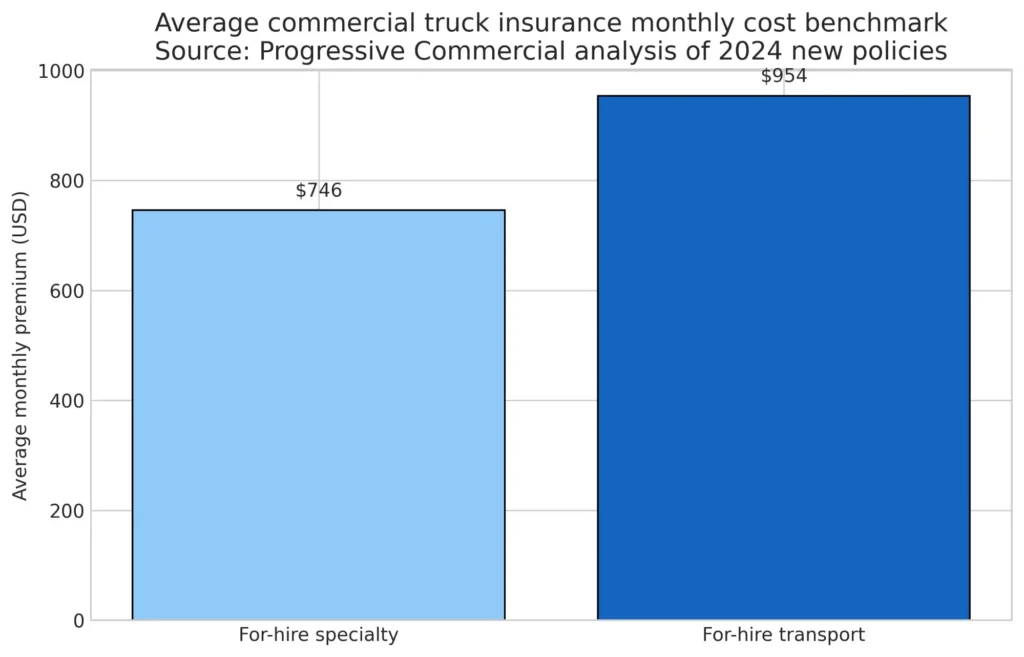

Then add your operating costs. Fuel remains the largest variable line item for most owner-operators, but it is not the only one. Insurance, permits, tolls, DEF, maintenance, tires, factoring or back-office fees, and parking or escrow deductions can all change your weekly break-even point. Progressive Commercial reports that the national average monthly cost for commercial truck insurance in its 2024 for-hire policy data ranged from $746 for specialty truckers to $954 for for-hire transport truckers, while actual rates vary with authority type, cargo, driving history, and operating radius [7].

Reserves are where many first-time buyers get into trouble. You need two separate cushions: an emergency operating reserve and a maintenance reserve. The emergency reserve protects you against slow pay, a weak freight week, or a registration delay. The maintenance reserve protects you against expensive but predictable wear items and surprise repairs. A reasonable starting habit is to set aside money every week or every mile, not only when something breaks.

| Cost bucket | Typical examples | Why it matters |

|---|---|---|

| Acquisition | Down payment, taxes, title, plates, dealer fees, immediate repairs | Determines how much cash you need before the truck produces revenue |

| Fixed monthly costs | Loan payment, insurance, ELD, accounting software, parking | Defines your minimum monthly burn rate |

| Variable operating costs | Fuel, DEF, maintenance, tolls, tires, washes | Moves with miles and freight type |

| Compliance and admin | Authority filings, IRP/IFTA/UCR-related costs, permits, drug and alcohol program | Can delay launch if not planned early |

| Reserves | Emergency fund and maintenance reserve | Keeps one breakdown from becoming a business failure |

A simple break-even method is to estimate your average all-in cost per mile, then compare it with your realistic loaded and blended revenue per mile. If your expected all-in cost lands at $1.85 per mile and your likely blended revenue is only $2.05, your margin is too thin for a buyer with little cash reserve. In that case, you either need cheaper equipment, better freight, or more cash before you buy.

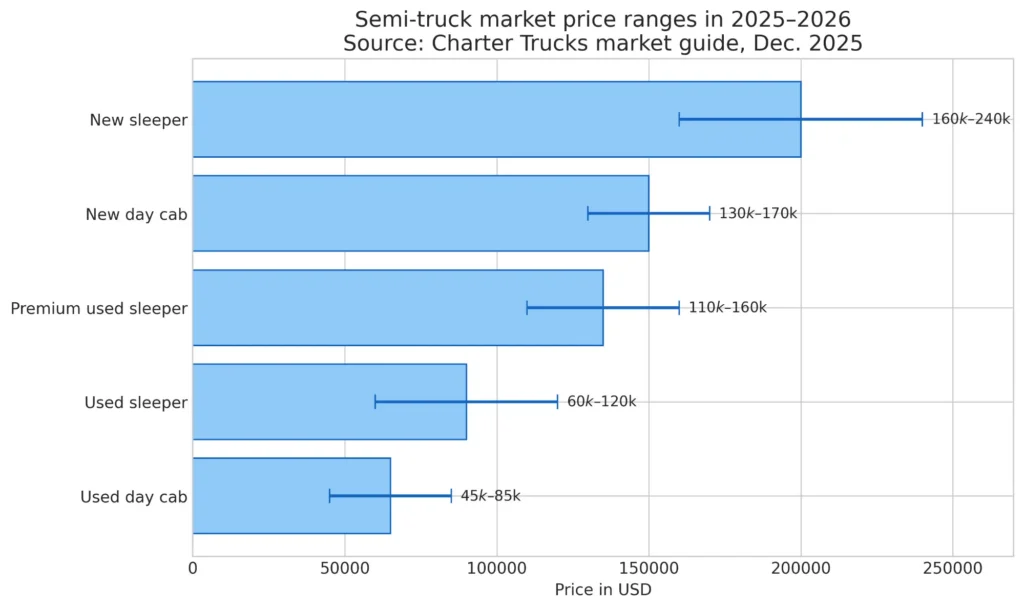

The current market range for trucks shows why budgeting must start with duty cycle and cash flow rather than aspiration. A December 2025 market guide from Charter Trucks places used day cabs at $45,000 to $85,000, used sleepers at $60,000 to $120,000, premium used sleepers at $110,000 to $160,000, new day cabs at $130,000 to $170,000, and new sleepers at $160,000 to $240,000, with premium long-haul sleepers climbing much higher [5].

How to buy a commercial truck

Understanding how to buy a commercial truck starts with matching specifications, condition, and price to the work the truck will actually do. That sounds obvious, but many first-time buyers shop backward. They find a truck they like, then try to make their business fit the truck. A better approach is to define the duty cycle first, then filter inventory.

For long-haul freight, engine torque, fuel capacity, driver comfort, and aerodynamic spec matter more because the truck spends long hours at highway speed and downtime is costly. For regional freight, maneuverability, weight, stop-start efficiency, and maintenance accessibility may matter more. Flatbed and heavy-haul buyers may prioritize axle configuration, frame strength, wheelbase, and PTO readiness. Reefer work may require stronger idle-management planning, electrical confidence, and dependable cooling support strategy.

Transmission choice also affects total ownership. Automated manual transmissions have become more common because they can support fuel efficiency, driver onboarding, and consistency, while manual transmissions may still appeal to drivers who value full control in certain terrain or specialty operations. Axle ratio, suspension setup, and wheelbase can influence both ride quality and MPG, so the best specification is rarely the most powerful or the most expensive. It is the one that fits your revenue model.

Is new, used, or certified pre-owned the best fit?

New equipment offers the strongest warranty protection and the lowest immediate repair risk, but it also creates the highest payment burden. Used equipment lowers the entry price and can improve cash flow if you buy well, but it increases the importance of inspections, service history, and reserve funding. Certified pre-owned inventory can sit in the middle, offering some inspection or warranty confidence at a price below new inventory.

| Option | Typical price range | Warranty position | Downtime risk | Best fit |

|---|---|---|---|---|

| New | Roughly $130,000 to $240,000+ for common specs [5] | Strongest factory or dealer warranty | Lowest early-life mechanical risk | Buyers with strong freight visibility, strong credit, and adequate reserves |

| Used | Roughly $45,000 to $120,000 for mainstream units [5] | Limited or none unless separately purchased | Higher, especially with weak history | Buyers prioritizing lower upfront cost and who can inspect carefully |

| Certified pre-owned | Often between mainstream used and new pricing | Usually some dealer-backed inspection or limited warranty | Moderate | Buyers wanting more confidence without a new-truck payment |

Mileage matters, but mileage alone does not tell the story. A late-model fleet-maintained truck with 450,000 miles and strong maintenance records may be a better buy than a poorly documented truck with 300,000 miles. Bankrate notes that some lenders are cautious about financing trucks older than 10 years or with more than 700,000 miles, which means mileage affects not only repair risk but also financing options [6].

Where should you shop?

Certified dealerships, fleet retirement channels, and reputable online listings are usually the safest starting points for first-time buyers. They tend to provide more documentation, better title clarity, and more realistic recourse if the truck is not as represented. Auctions and private-party purchases can create strong value for experienced buyers, but they are less forgiving if you miss a major mechanical issue or paperwork problem.

The minimum document package to request includes the maintenance history, fault-code scan or ECM report, title status, accident information, and any oil analysis or warranty details. If the seller hesitates to provide maintenance records or seems vague about recent aftertreatment work, assume risk is being transferred to you and price the truck accordingly.

First-time semi truck buyer program

A first-time semi truck buyer program usually refers to lender or dealer programs designed for applicants with limited owner-operator history, thinner business credit, or less cash available for a large down payment. These programs can sometimes help buyers get into equipment sooner, but they are not magic. The tradeoff is often a higher rate, shorter list of eligible trucks, or stricter documentation requirements.

Most programs focus on the same core questions: How long have you held your CDL? Do you have verifiable driving experience? Are you buying through a business entity? Can you show proof of income, settlements, or contracts? How much money are you putting down? The better you answer those questions, the more choices you usually have.

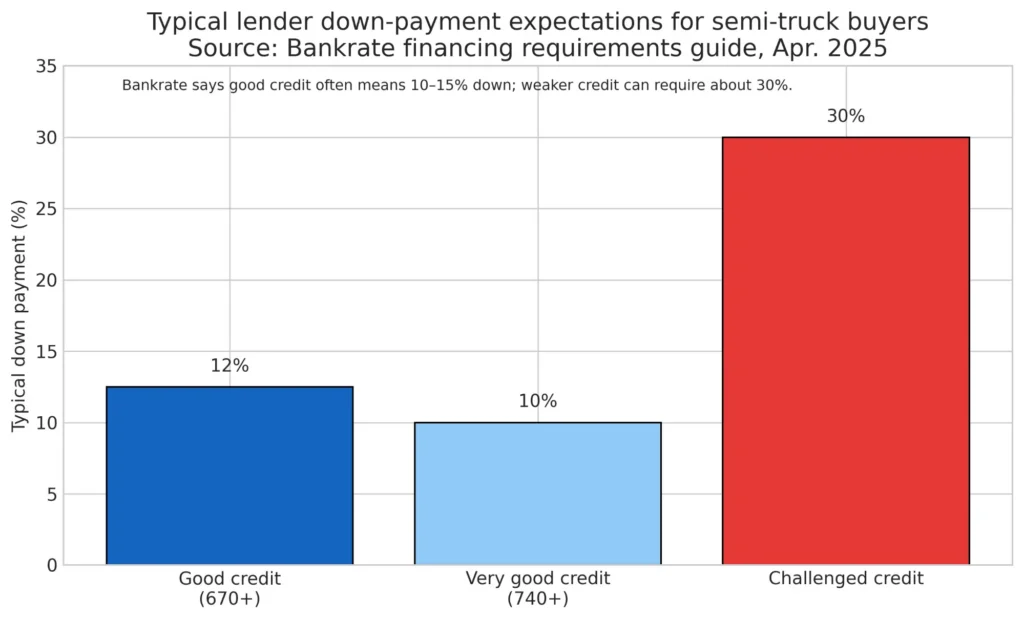

Bankrate reports that credit scores of 670 and above are generally considered good for financing, while scores above 740 may qualify for stronger rates. It also says borrowers with good credit often see down-payment requests in the 10% to 15% range, while weaker credit profiles may face requirements near 30% [6]. That is why improving credit utilization, fixing report errors, and saving additional cash before applying can materially change your buying options.

SBA-backed financing can also be relevant when the truck purchase is part of a larger business plan. SBA states that its 7(a) program can be used for purchasing equipment, working capital, and refinancing debt, with maximum loan amounts up to $5 million for eligible small businesses [3]. While many owner-operators still use standard equipment financing rather than SBA-backed loans, SBA guidance is useful if you are building a more formal business structure or combining truck financing with broader startup needs.

Loan or lease for your first truck?

A loan usually gives you ownership, equity buildup, and fewer long-term usage restrictions once the note is paid. A lease may lower the initial cash requirement or create an easier path into a newer truck, but you need to examine mileage limits, residual value terms, early termination provisions, maintenance obligations, and what happens if freight slows down.

In plain terms, the right question is not “Which is cheaper this month?” The right question is “Which structure leaves me with the best cash flow, the lowest downside risk, and the fewest surprises for the kind of operation I want to run?” For many first-time buyers, the answer depends on their reserve strength and whether they need the carrier support that sometimes comes with lease-on arrangements.

| Qualification factor | What lenders often want to see | Why it affects approval |

|---|---|---|

| CDL and experience | Time with CDL, clean driving history, recent commercial driving experience | Reduces perceived operational risk |

| Income proof | Settlements, W-2s, tax returns, or contracts | Supports repayment capacity |

| Business documents | LLC or corporation paperwork, EIN, business bank account | Shows business readiness |

| Credit profile | Personal score, utilization, recent delinquencies | Influences rate and down payment |

| Cash down | Often stronger terms with more cash injected | Lowers lender risk and monthly payment |

Programs worth asking about include deferred first payment, included limited warranty, maintenance credits, pre-qualification with a soft inquiry, and the rate-lock period. These details can matter more than a flashy headline rate if your truck will not be ready for dispatch immediately.

Step-by-step: how to purchase a semi truck

The cleanest buying process is sequential. When buyers compress steps or skip independent verification, they usually pay for it later in repairs, delays, or financing frustration.

Step 1: Define your business model and lanes. Decide whether you will lease on to a carrier or run under your own authority. Specify your target freight, average haul length, operating regions, and any customer or broker requirements before you shop.

Step 2: Build your budget and TCO. Estimate acquisition cost, payment range, insurance, fuel, maintenance, permits, and reserves. Decide what monthly payment still leaves breathing room when rates soften.

Step 3: Check personal and business credit. Review your reports, dispute obvious errors, reduce utilization where possible, and organize documents that show income and business readiness.

Step 4: Get pre-qualified. Compare equipment lenders, dealer finance options, credit unions, and, if relevant, SBA-backed lending routes. Ask about down payment, truck age limits, mileage caps, required insurance, and whether pre-qualification uses a soft inquiry.

Step 5: Shortlist trucks that match your duty cycle. Match engine, transmission, axle ratio, wheelbase, and emissions history to the work you plan to run. Avoid buying a truck just because it looks like a bargain.

Step 6: Run history and paperwork. Request maintenance logs, title status, ECM information, oil analysis, accident history, and evidence of major component work. If you cannot confirm history, reduce your offer or move on.

Step 7: Inspect and test drive. Conduct a cold start, road test, brake inspection, tire review, and aftertreatment check. Hire an independent mechanic if you do not have deep heavy-duty diagnostic experience.

Step 8: Negotiate from findings, not emotion. Use documented defects, missing records, tire condition, warranty gaps, and upcoming maintenance to negotiate price or repairs.

Step 9: Bind insurance and complete paperwork. Lenders and carriers may require proof of insurance before funding or dispatch. Make sure the purchase agreement, title transfer, taxes, warranty forms, and any lien documentation are correct.

Step 10: Register and launch correctly. FMCSA says companies subject to safety registration must obtain a USDOT number, and interstate for-hire carriers transporting federally regulated commodities generally also need operating authority [1] [2]. State DMV and motor carrier agencies then control title, registration, and other state-specific steps [8].

Financing and budgeting essentials

Financing is where many good truck purchases become bad business decisions. The issue is usually not approval. It is payment structure. A truck can be financeable and still be a poor fit for your cash flow.

Use your rolling three-month revenue history, or a conservative projected revenue model if you are new, to set a payment comfort zone. The payment should leave enough margin to absorb insurance, fuel spikes, maintenance, and at least a few slow weeks. If the deal only works when everything goes right, it is too tight.

The same logic applies to term length. A longer term may improve monthly cash flow but increase total interest cost and keep you upside down on the truck for longer. A shorter term cuts total interest but may raise the payment too far. Balance the payment against realistic revenue, not best-case revenue.

Two buyer profiles show how this plays out in practice. Buyer A is a company driver with excellent credit, a long CDL history, and a dedicated regional opportunity. Buyer A may be able to justify a later-model certified or newer truck because stronger credit lowers the down payment burden and freight visibility reduces payment risk. Buyer B is a first-time owner-operator with average credit, limited cash, and spot-market exposure. Buyer B is often safer in a well-documented used truck with lower acquisition cost, even if the truck is less glamorous.

IRS guidance also matters in budgeting because depreciation strategy can change your year-one cash planning. IRS states that Section 179 allows eligible businesses to deduct the cost of certain property, including qualifying equipment, when first placed in service, subject to applicable limits and tax circumstances [4]. That does not mean you should buy a truck for the tax write-off, but it does mean you should talk with a tax professional before year-end if the truck purchase is part of a broader business strategy.

What should you inspect and test drive before buying?

A used truck purchase should be treated like a mechanical audit. The inspection is not a formality. It is part of the valuation process. The better your inspection, the less likely you are to overpay for someone else’s deferred maintenance.

Start with the engine and aftertreatment system. Check for visible leaks, blow-by, hard cold starts, active and inactive fault codes, and evidence of recent DPF, DOC, or SCR issues. Ask whether the truck has had recent forced regens, injector work, turbo replacement, or sensor replacements. Emissions-related downtime can erase the savings of a cheap truck very quickly.

Move next to the driveline, suspension, brakes, and tires. Look for U-joint play, ride-height issues, cracked bushings, leaking shocks, uneven tire wear, air leaks, and brake lining condition. Tire wear patterns can reveal alignment problems or suspension wear that is not obvious in a quick walkaround.

The road test should include a true cold start if possible, a shifting evaluation, a loaded-feel acceleration test if permitted, brake response, steering feel, temperature stability, and vibration review. HVAC and electrical systems matter more than many first-time buyers realize because wiring, battery, and charging problems create repeat downtime and can affect safety systems.

| Inspection area | What to verify | Why it matters |

|---|---|---|

| Engine and aftertreatment | Blow-by, leaks, fault codes, DPF/DOC/SCR condition | Major repair exposure and downtime risk |

| Driveline and suspension | U-joints, bushings, shocks, ride height | Ride quality, tire life, and drivability |

| Brakes and tires | Tread depth, air leaks, lining thickness, even wear | Immediate safety and near-term replacement cost |

| Electrical and HVAC | Batteries, alternator output, harness condition, HVAC function | Reliability, comfort, and dispatch readiness |

| Cab and frame | Rust, repairs, body integrity, corrosion | Structural condition and resale value |

| Documentation | ECM data, service records, oil analysis, title status | Confirms whether the story matches the truck |

If you are not comfortable reading the truck yourself, hire an independent mechanic and pay for an oil analysis. That cost is trivial compared with the cost of buying the wrong unit.

What insurance, registration, and compliance steps come next?

Insurance should be lined up before funding and certainly before dispatch. Depending on how you operate, you may need primary liability, cargo, physical damage, bobtail or non-trucking liability, occupational accident or workers’ compensation considerations, and additional filings. Progressive notes that federal filing requirements often bring minimum combined single limit expectations of $750,000 or $1,000,000, depending on cargo and vehicle type [7].

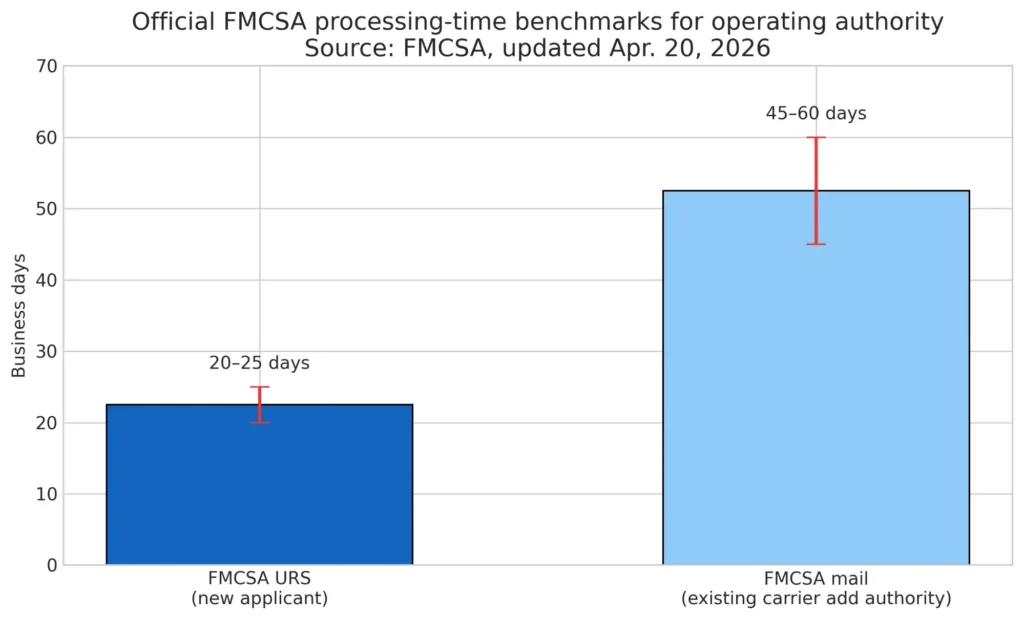

Registration timing is another reason to plan ahead. FMCSA’s registration guidance says companies may need both safety registration and operating authority registration, and its operating-authority page notes that new-applicant URS filings may take around 20 to 25 business days, while certain mailed authority additions for existing carriers can take 45 to 60 business days [1] [2]. That means you should not assume you can buy a truck on Friday and be fully ready for interstate for-hire operations on Monday.

State paperwork matters too. California DMV, as one state example, says commercial vehicles used primarily to transport property or people for hire, compensation, or profit must be registered, and it points operators to additional commercial vehicle, IRP, and motor-carrier resources for specific registration obligations [8]. Your own state may use different forms, weight declarations, deadlines, and permit rules, so verify local requirements before closing.

In practice, many interstate buyers also work through related steps such as IRP, IFTA, UCR, ELD setup, a drug and alcohol testing program where required, and carrier-safety onboarding. The key takeaway is that compliance is not a single form. It is a workflow, and the truck purchase should be timed around it.

How do you set up the truck for profitability after purchase?

A good purchase can still become an unprofitable operation if the truck is not managed correctly after delivery. Profitability starts with maintenance discipline. Establish preventive-maintenance intervals immediately, decide where you will source parts, and build a relationship with a shop network before the first major breakdown. If you wait until you are stranded, every repair decision becomes more expensive.

Fuel strategy is the next big lever. Track MPG from day one, compare routes and fuel networks, and review idle time and driving habits. A small MPG improvement over a long-haul year can matter more than a marginal interest-rate improvement on the note.

Load sourcing and back-office systems also deserve attention. Decide whether you will rely on a load board, direct shipper outreach, broker relationships, or a dispatcher. Then pair that with bookkeeping that tracks revenue by lane, cost per mile, maintenance trend, and quarterly tax obligations. SBA planning guidance supports this broader business-first view, because financing decisions are only as strong as the business systems behind them [3].

Final purchase-day checklist

Before you take possession, pause and confirm the practical details one more time. Verify the VIN, purchase agreement, title status, lien information, tax treatment, warranty paperwork, insurance binder, registration path, and any repairs promised by the seller. Confirm you have both keys, manuals if available, current mileage, and a written list of included accessories or installed equipment.

Most important, make sure your first 30 days are funded. That means you have cash left for fuel, insurance, maintenance, permits, and slow pay, not just the down payment. The best truck purchase is the one that lets you start operating from a position of control rather than immediate financial pressure.

In the end, understanding how to purchase a semi truck comes down to four disciplines: plan your business model clearly, budget beyond the payment, inspect more deeply than the seller expects, and complete compliance before you count on revenue. If you follow that order, you give yourself the best chance to buy with confidence instead of learning expensive lessons on the road.

Frequently Asked Questions (FAQ): The Path to Buying a Truck

How much does it cost to purchase a semi truck today?

Current market ranges vary by age, configuration, and sleeper setup, but recent 2025 market guidance places used day cabs around $45,000 to $85,000, used sleepers around $60,000 to $120,000, and common new sleepers around $160,000 to $240,000 [5]. Your actual budget should also include taxes, registration, insurance, immediate maintenance, and reserve funding.

Is it better to buy a new or used semi truck for owner-operators?

It depends on cash flow and downtime tolerance. New trucks reduce early repair risk and usually provide better warranty protection, while used trucks reduce the upfront cost and may be the safer business choice for buyers who want a lower payment and can fund inspections and repairs properly.

What credit score do I need to buy a commercial truck?

There is no universal minimum, because lenders vary. Still, Bankrate reports that scores of 670 and above are generally considered good for semi-truck financing, while scores above 740 may lead to better terms [6]. Stronger credit usually improves both rate and down-payment flexibility.

How much is a typical down payment for a semi truck?

For many borrowers, a typical range is around 10% to 15% with stronger credit, while weaker credit can push the requirement closer to 30% [6]. Truck age, mileage, and business history also influence the lender’s final requirement.

What is a first-time semi truck buyer program and how do I qualify?

It is usually a lender or dealer program built for applicants with limited owner-operator history. Qualification often depends on CDL tenure, verifiable income, business documents, credit quality, and cash down. Some programs also add features such as deferred first payment, limited warranty coverage, or maintenance credits.

Should I finance or lease my first semi truck?

Financing usually gives you ownership and long-term equity, while leasing may lower the barrier to entry or help you access newer equipment. The better choice depends on your reserves, the freight model you will run, and how the agreement handles mileage, maintenance, and end-of-term obligations.

What mileage is too high when buying a used semi truck?

There is no single cutoff, because service history matters as much as mileage. However, some lenders limit financing on trucks with more than 700,000 miles or older than 10 years, which makes those thresholds important even before you think about repairs [6].

What inspections are non-negotiable before I purchase a semi truck?

At minimum, review engine and aftertreatment condition, brakes, tires, driveline, suspension, electrical system, ECM information, maintenance history, and title status. For a used truck, an independent mechanic report and oil analysis are often worth every dollar.

What insurance do I need to drive as an owner-operator?

The answer depends on whether you are leased to a carrier or operating under your own authority. Common coverages include primary liability, cargo, physical damage, and bobtail or non-trucking liability. Cargo type and operating authority affect required limits and premium levels [2] [7].

What permits and registrations are required for interstate operation?

FMCSA states that companies subject to safety requirements need a USDOT number, and interstate for-hire carriers hauling federally regulated commodities generally need operating authority as well [1] [2]. Beyond FMCSA registration, state and multi-state requirements may include title work, apportioned registration, fuel tax registration, and related operating permits depending on how and where you run.

How do I estimate my cost per mile and break-even rate?

Add fixed monthly costs such as payment and insurance, convert them to a per-mile figure based on realistic monthly miles, then add variable costs such as fuel, maintenance, tires, tolls, and DEF. Your break-even rate is the all-in cost per mile plus the profit margin and reserve contribution you need to stay healthy.

Where is the best place to buy a commercial truck safely?

For first-time buyers, the safest places are usually certified dealerships, reputable fleet-retirement sellers, and established online platforms that provide documentation and clear title history. Private-party deals and auctions can produce value, but they are far less forgiving if you miss a major defect.

References

[1] Federal Motor Carrier Safety Administration. (2025). Getting Started with Registration. https://www.fmcsa.dot.gov/registration/getting-started

[2] Federal Motor Carrier Safety Administration. (2026). Get Operating Authority (Docket Number). https://www.fmcsa.dot.gov/registration/get-mc-number-authority-operate

[3] U.S. Small Business Administration. (2026). 7(a) loans. https://www.sba.gov/funding-programs/loans/7a-loans

[4] Internal Revenue Service. (2025 review). Depreciation expense helps business owners keep more money. https://www.irs.gov/newsroom/depreciation-expense-helps-business-owners-keep-more-money

[5] Charter Trucks. (2025). How Much Does a Semi Truck Cost in 2025–2026? A Realistic Price Range for Buyers. https://chartertrucks.com/blog/how-much-does-a-semi-truck-cost-in-2025-2026/

[6] Bankrate. (2025). Semi-Truck Financing Requirements. https://www.bankrate.com/loans/small-business/semi-truck-financing-requirements/

[7] Progressive Commercial. (2026). Commercial Truck Insurance Cost. https://www.progressivecommercial.com/commercial-auto-insurance/truck-insurance/commercial-truck-insurance-cost/

[8] California Department of Motor Vehicles. (2026). Commercial Vehicle Registration. https://www.dmv.ca.gov/portal/vehicle-registration/new-registration/commercial-vehicle-registration/